Saeid Khoshrou, Deputy General Manager of National Iranian Oil Company's International Affairs for Product Marketing, addressed the 2016 Asia Energy Cooperation Forum in Chongqing about the demand for crude oil in Asia. The following is an excerpt of his address.

Asia crude Demand at a glance

Asia is home for some of the biggest crude oil consuming countries. Asia Demand growth pace is faster than any region else and amounted to more than 1 million barrel per day in the first five months year on year. China is the second largest economy in the world with an apparent demand of around 12 mb/d. As the top Asian importer of crude oil, China has imported some 8 mb/d recently where more than 52% came from Middle East. Indian oil demand continued on its growth path and added to 280 kb/d y-o-y, while the country as the second Asian market for crude oil, imported around 4 mb/d from which more than 60% produced in Middle East. South Korea oil demand is reported to increase 250 kb/d in the last five months compared to the same period last year. According to the latest data from Korea National Oil crop., the country imported about 3 mb/d on average, an increase of 14% m-o-m. Going to Japan as the third oil consumer in Asia, the country’s oil import has decreased steadily over the years. However, it is still one of the main destinations for crude came from M.E with an import of around 3.5 mb/d. Having this picture in mind, it is not surprising that Middle East Producers are increasingly focusing on Asia Market.

Iran is well-known by its practical and potential role in the oil and gas market. 35tcm gas and 157 mmb crude reservoir has brought a strategic position to this country. Iran has been a key member of OPEC with the current crude production of around 3.9 mb/d and more than 2.5 mb/d as export. Iran has boosted crude oil production and exports due to the new political environment in the country and international relationship.

Iran aimed to raise its oil output to 4 million b/d by end of this year and to 4.8 million b/d in five years. Achieving this goal is not so far and it gives the country a very specific opportunity to make a more strategic relationship with Asian oil consuming countries.

China, imported an average of 7.92 million b/d, of crude oil in May, surging 38.7% year on year from a low base in the same month of last year. Recently, Tehran and Beijing have signed a deal that is indicating Iranian crude supply to China will rise to more than 1 million b/d. This cooperation agreement includes exploration, enhancement of recovery and development [of oil and gas], manufacturing oil and gas equipment and also different investments in these areas. Iran's crude used to cover 11% of China's oil needs, and it can easily to reach that peak very soon. China's crude oil imports from Iran peaked at 557,413 b/d in 2011 but fell to 430,585 b/d over 2013 before recovering to 534,506 b/d in 2015. It is currently around 800,000 b/d and is planned to continue on growing to 1 mb/d.

Over the first five months, India's oil products demand rose more than 12% year on year to an average of 4.23 million b/d. The International Energy Agency in the Oil Market Report released in May named India as a star performer based on first quarter demand, which was up 400,000 b/d year on year and accounted for almost 30% of the global increase. This provides further support for the argument that India is taking over from China as the main growth market for oil.

Indian crude oil import is around 4.1 mb/d and from which more than 300 kb/d comes from Iran. India’s crude oil import from Iran is doubling and is going to boost to over 400 kb/d in near future.

According to METI, Japan's total crude imports in April averaged at 3.47 million b/d, up 3.4% from a year ago, marking the first year-on-year increase in monthly crude imports in five months. Japan used to import an average 120 kb/d of crude from Iran before lifting the sanctions. Japanese crude imports from Iran have shown more fluctuation over March-April than other months because of the change in financial year which affects insurance renewals for vessels. However the latest news shows that Iran is going to increase its oil exports to Japan drastically and have a new record of around 250 kb/d in very near future.

South Korea’s crude oil imports averaged about 3 mb/d recently and imports of Iranian crude averaged 237 kb/d almost double the level seen a year earlier. South Korea and Iran have agreed to triple their annual trade to $18bn (£12.2bn) as the two countries sign several business deals. South Korea as the world's fifth-largest oil importer remains one of the major crude importers for Iran.

China, India, Japan and South Korea are importing some 18 mb/d of crude oil. Iran can easily take a share of 12% to meet this requirement, in such case 2 mb/d of Iranian crude oil is going to destined for Asia. That’s the reason make someone confident in saying that there is a really huge potential market between Iran and Aisa.

Condensate Supply - Demand

Apart from crude production, non-crude liquids production by OPEC averaged 6.6 million b/d in 2015, and it is forecast to increase by 0.3 million b/d in both 2016 and 2017, mostly led by increases in Iran and very rarely in Qatar. Non-crude liquids production is mainly including of condensate production. The condensate production is mostly dependent on development and the richness of the gas reserve and in Asia the supply of condensate rallied considerably by developing the world's largest gas field, shared between Iran and Qatar. Hence, Qatar and Iran are the key condensate producers. Although the main source of condensate in both Qatar and Iran is the South Pars / North Dome field, these two countries are also producing condensate from their other gas field. The story of condensate production from this largest gas field is not very old and since then market players started to construct distillation units which are planned to use condensate as their feedstock in both Middle East and Asia Pacific. New petrochemical units were designed to use condensate as feedstock in order to have more flexibility. Furthermore, splitters were designed and constructed to split light hydrocarbons of condensate and thereupon, the market demand for gas condensate were expanded.

The South Pars / North Dome field is a natural gas condensate field located in the Persian Gulf. It is the world's largest gas field, stradles between Iran and Qatar. The Iranian part holds 18 billion barrels of condensate in place of which some 9 billion barrels are believed to be recoverable, while Qatari section believed to contain some 30 billion barrels of condensate in place and at least some 10 billion barrels of recoverable condensate. The South Pars Field was discovered in 1990 by NIOC. The Pars Oil and Gas Company, a subsidiary of NIOC, has jurisdiction over all South Pars-related projects. Gas production started from the field in December 2002 to produce 1bscf/d of wet gas. Gas is sent to shore via pipeline, and processed at Assaluyeh to produce condensate and LPG.

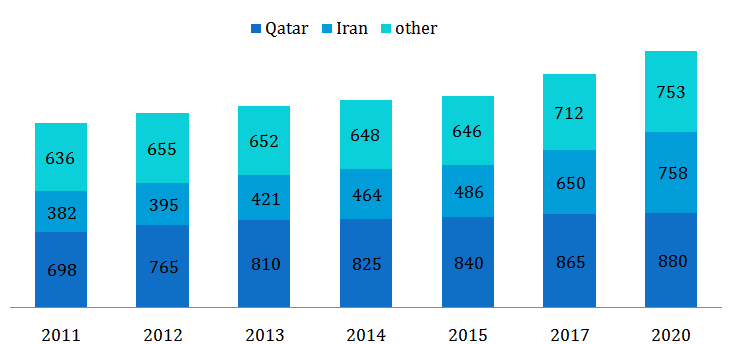

Total Qatari condensate production is now 850 thousand barrels per day and will be remained unchanged by the end of the decade. While in Iran production of S.P. condensate alone is planned to increase during the coming periods reaching 810 thousand barrels per day. The other types of condensate production in Iran are altogether around 150 thousand barrels per day.

In Iran, the under development phases of S.P. gas field mainly consist of 24 phases. Generally each phase is planned to have nominal production of 40 thousand barrels per day. At the current situation, 15 phases are under operation and totally are producing 530 thousand barrels per day. Looking forward, total production of S.P. Condensate is expected to be around 650 thousand barrels through 18 phases during a year from now. Moreover, with the completion of all 24 phases of the S.P. refinery, total production is expected to be more than 810 thousand barrels per day. Hence Iran is exclusively going to absorb the new capacity of condensate demand in the area.

Condensate production from M.E. and outlook (kb/d)

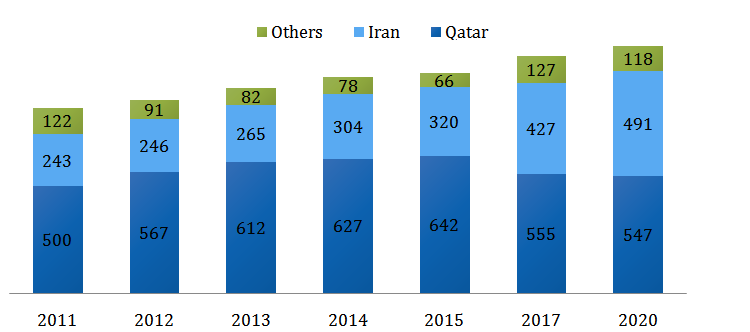

On the demand side, condensate can be considered a base material, equivalent to crude for refining or feedstock in petrochemical units and splitters. Splitters are simple distillation units which are planned to split light hydrocarbons. Both petrochemical units and splitters are designed to use condensate as whole of their feedstock, while refineries have to use a blend of condensate and crude as feedstock with a ratio 1 to 9. Thus petrochemical units and splitters are major consumers of condensate. The current petrochemical and splitting capacity in Asia Pacific and Middle East is totally around 1/8 million barrels per day. It is expected to see condensate refining capacity additions in both Middle East and Asia Pacific regions during the coming months. 120 kb/d Persian Gulf Star 1 in Iran and 140 kb/d Ras laffan 2 in Qatar are going to come on stream in the near future and Qatari splitter will reduce the country’s exportable condensate by around 140 kb/d. Going to Asia pacific, 130 kb/d Hyundai Lotte splitter in South Korea is planned to start operation from end of third quarter 2016. With consider to the expected domestic demand for Qatari Condensate, Qatar condensate availability for export will be limited.

Condensate Export from M.E. and outlook (kb/d)

The condensate demand mainly originates from Asia in particular South Korea and Japan, while the main source which meets this demand is Iran and Qatar as explained. In South Korea total splitting capacity is around 400 thousand barrels per day and is going to be decreased by 100 kb/d reaching to 500 kb/d in September 2016. Iran is already covering a large share of South Korean condensate requirements and also there are some signed agreements between South Korea and Iran to deliver S.P. condensate to the new splitters coming on stream in the South Korea. This story is happening not only in South Korea but also in other Asian condensate importers such as Japan, Singapore, China and UAE. Looking forward, Iran is likely the leading supplier in South Korea and among other newcomers market.

Iranian S.P. Condensate boom days are coming on the back of new production additions. The development plan of the rest phases of the S.P. gas field aims to help Iran to be the leading market in supply of condensate. As well as Supply side opportunities in Iran, there are also new opportunities in demand side. Emerging consuming units in Asia and also growing interest among refineries to use condensate as any light crudes will support S.P. Condensate demand in both splitting and refinery units in Middle East and more than that in Asia Pacific. Not only condensate, but also LPG production will improve due to the incoming development of S.P. gas field.

Asia LPG Supply- Demand

The non-refinery LPG production by OPEC Members is around 80 million tons. While, non- OPEC LPG production is near to 100 million tons. Roughly 43% of total non-refinery LPG production is from OPEC countries and this is while Middle East covers 37 million tons of OPEC LPG production. Based on OPEC’s production targets, its production is expected to grow during the next periods and part of the gain is due to Iran incremental LPG production.

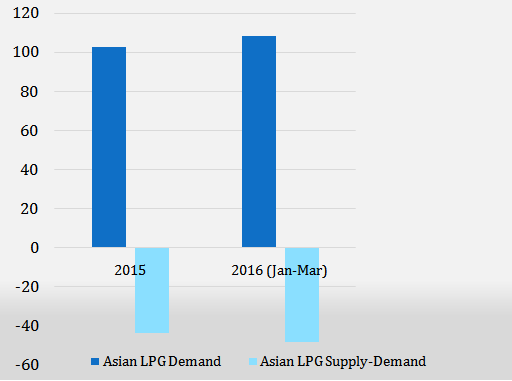

According to the latest statics, Asia LPG Demand is around 105 million tons this year and the LPG market will be the most growing LPG market in the world in both consumption and production side. China, Japan, India and Indonesia will play more important role in the consumption market while Middle East producers are leading LPG production.

Asia LPG Supply- Demand (mt)

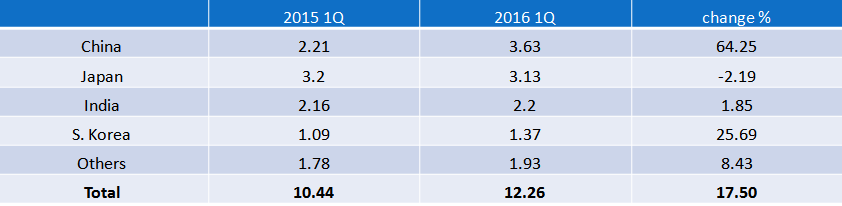

On the demand side, there are two sources which support this increasing volume in the futures, first is residential consumption and the second and is petrochemical usage. Total import volume in Asia for the year 2014 was around 41 million tons and for 2015 was around 44.2 million tons which shows 7 to 8 percent increase in import figures. As per FGE’s forecast annual growth for LPG consumption in the Asian countries between 2015-2020 would be around 4.1% annually and for the period 2020 -2030 would be around 1.1%. China's LPG imports topped 12 million tones in 2015 and put it on course to overtake Japan as the world's largest LPG importing nation. Moreover, India and Indonesia are two other growing Asian LPG consumers.

China imported more than 6.5 m/t of LPG in the first five months of this year, a remarkable increase of about 56 % year on year. This increase is largely attributed to growing LPG demand from propane dehydrogenation (PDH) units. The country’s dependency on imported LPG has increased to around 40%, from 37% in 2015 and 24% in 2014.

Selected Asian Countries LPG Imports (mt)

Furthermore, there is an advantage for countries like Iran to invest and focus on Asian LPG market as main export outlet due to the freight aspects.

On the supply side, Middle East countries are leading the market and the majority of Middle East LPG exports head to Asia and in particular India, Japan, Indonesia and China. Middle East is totally producing 37 million tons of LPG per year. Iran With small difference from its competitors is in fourth place among Middle East exporters after Qatar, Saudi Arabia and UAE. Iran’s LPG production totaled 6.5 million in 2015. However, it is expected that Iranian LPG production and accordingly its export will considerably rally during the upcoming period. This will happen mostly on the back of developing the world's largest gas field shared between Iran and Qatar. Iran aims to produce more than 12 million tons of LPG each year by the year 2025.

As of fourth quarter of 2015, there are sixteen phases in operation in South Pars gas field, with ten of them producing LPG. The eight further phases are currently in the development stage (with varying degrees of progress) and are expected to start up production between 2016 and 2025.

In 2015, the exportable quantity of LPG from Iran is around 13 percent of total volume exported from Middle East. The total volume of Iranian seaborne exports between January and December was round 4.5 million tons. This volume is already significantly higher than 2014, which was estimated at 3.2 million tons. This hike already highlights the current activity of the S.P. developments and its potential. Looking forward, Iranian LPG exportable volume will reach to 9 million tons by the year 2025.

All in all, seaborne exports are estimated to grow significantly in the forthcoming years, but the final export volume will be a function of the investment activity in the country, the further development of S.P. gas field and the startup timing of the new petrochemical consuming facilities.

All things considered, Iran energy investment may plan to Define Future LPG Supply- Demand. The current exportable volume (5 million tons) and forecasted quantity (9 million tons) will be resulted Iran to be in a more powerful position in the LPG market.

With this general picture in mind, you can see why it is important for Asian countries to have a more strategic relationship. Asia demand for Crude oil, Condensate and LPG is growing at a fast pace and Iran growing production should be considered as an opportunity for these countries.

References

- BP Statistical Review of World Energy; June 2016

- FGE; MENA Gas Monthly Report; May & June 2016

- Poten & Partners; LPG in World Markets; Apr & May 2016

- FGE; Asia Pacific Petroleum Monthly; Apr & May 2016

- FGE; Asia Pacific Data book; Spring 2016

- FGE; Middle East Petroleum Data book; Spring 2016 & 2014

- Petroleum Intelligence Weekly (PIW); NOs 5,21 & 22

Your Comment