On July 5, 2025, the same members met virtually and, citing strong economic growth and tight market fundamentals, agreed to boost output by 548,000 bpd in August 2025, exceeding expectations of 411,000 bpd. This move supports the phased return of previously cut supply and aims to meet robust summer demand in the Northern Hemisphere. The increase is adjustable, with flexibility to pause if needed. Members also pledged to compensate for overproduction since January 2024 and will continue monthly meetings, with the next set for August 3, 2025, to review September output.

OPEC+ Decision and Context

On July 5, 2025, eight OPEC+ member countries agreed to increase production by 548,000 barrels per day (bpd) in August 2025, relative to July’s mandated output levels. This single-step increase, equivalent to four standard monthly increments, advances the group’s December 2024 roadmap to gradually reinstate 2.2 million bpd of voluntary production cuts beginning in April 2025. Notably, the August adjustment exceeded market expectations of a 411,000-bpd rise, marking a significant departure from the incremental increases implemented in May, June, and July, and surprising many industry analysts.

The decision was underpinned by resilient market fundamentals and a strengthening global economic outlook. Suhail Al-Mazrouei, UAE Minister of Energy, emphasized that global markets have effectively absorbed additional OPEC+ supply since spring 2025 without triggering inventory buildups, underscoring robust underlying demand: “Even with higher production over recent months, we have not seen notable inventory accumulation, evidence that the market continues to require these barrels.” Declining oil inventories, particularly during the peak summer travel season in the Northern Hemisphere, reinforced this assessment. Additional demand pressures stem from elevated air conditioning needs in the Middle East and increased crude stockpiling by China. These factors have contributed to tighter market conditions, with Brent crude futures rising from approximately $58 per barrel in April 2025 to around $68 by August 2025.

Motivations for the Decision

Several factors underpinned OPEC+’s production increase:

- Seasonal Demand Surge: The summer driving season in the Northern Hemisphere drives substantial fuel demand. The August increase leverages this demand to ensure market stability.

- Robust Market Fundamentals: Low oil inventories reflect a balanced supply-demand dynamic, providing OPEC+ an opportunity to boost production without destabilizing markets.

- Market Share Competition: Rising output from non-OPEC producers, such as the United States, Canada, Brazil, and Guyana, prompted OPEC+ to increase supply to maintain its market share.

- Overproduction Compensation: Some members of DOC, who exceeded production quotas, faced pressure to compensate. The August increase facilitates accelerated compensation for overproduction since January 2024.

- Chinese Stockpiling: China’s crude oil stocks rose by 82 million barrels (approximately 900,000 bpd) in Q2 2025, driven by commercial or strategic energy security motives, supporting market tightness.

OPEC+ underscored the importance of flexibility, stating that production increases could be paused or reversed in response to changing market conditions, allowing for swift adjustments to shifts in demand or geopolitical developments.

Market Implications and Analysis

The OPEC+ production increase of 548,000 bpd, above market expectations—has significant implications for global oil markets, which remain tight despite the planned hikes. Key factors sustaining tightness include:

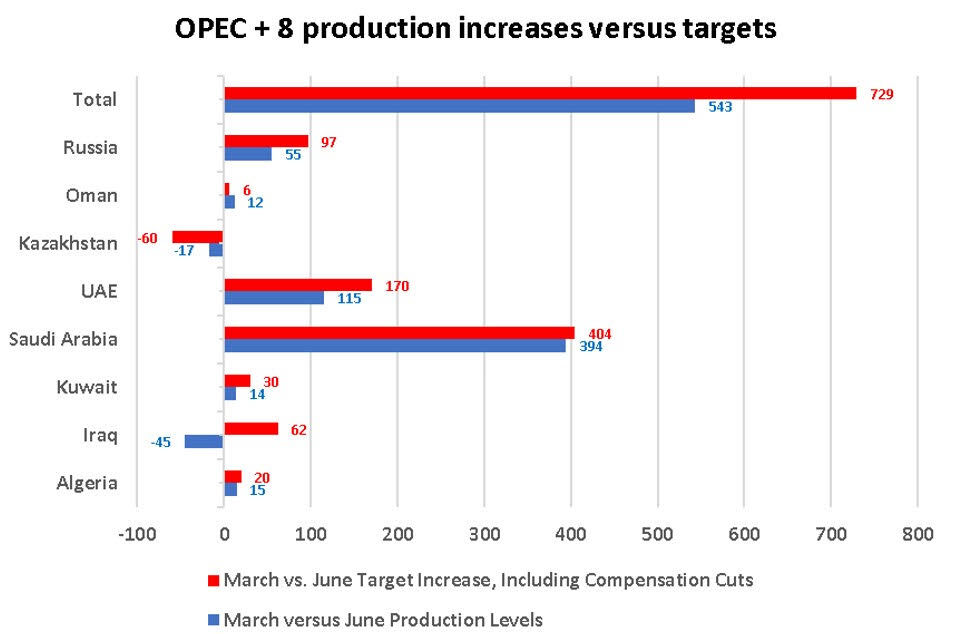

Output Shortfalls: Several members have failed to meet output targets. As a result, actual increases from April to June totaled only 540,000 bpd, well below the 960,000-bpd target.

Rising Prices: Brent crude has risen from $58 in April 2025 to around $68, supported by a backwinded market structure, with near-term prices trading at a $2.74 premium over six-month futures in August.

Strong Demand: Higher refinery runs, peak summer cooling demand in the Middle East, and Chinese stockpiling have absorbed additional supply, preventing inventory buildups.

Low Inventories: OECD crude stocks remain below average, European inventories were 9% below the five-year norm (394 million barrels in May), and U.S. stocks were also below average (419 million barrels in June), providing price support.

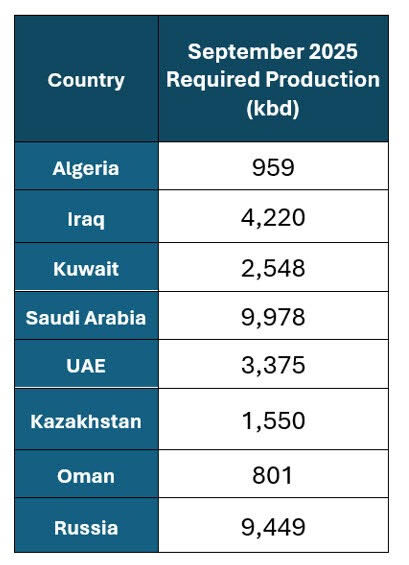

Looking ahead, analysts expect softer demand in fall 2025 as summer consumption wanes, potentially leading to inventory builds and downward pressure on prices, already down 8.5% since January 2025. Despite this, OPEC+ to approve another ~550,000 bpd increases for September at its August 3 meeting, completing the phase-in of the 2.2 mbpd voluntary cuts and incorporating a 300,000-bpd quota increase for the UAE, reflecting its expanded capacity. This highlights OPEC+’s strategy to adapt to market conditions and enhance competitiveness, though limited spare capacity outside Saudi Arabia and the UAE may constrain actual output growth.

Commitment to Compliance and Monitoring

The eight OPEC+ countries reaffirmed their commitment to the Declaration of Cooperation, including the voluntary production adjustments agreed upon during the 53rd Joint Ministerial Monitoring Committee (JMMC) meeting on April 3, 2024. They committed to fully compensate for any overproduction since January 2024 and have submitted updated compensation plans to the OPEC Secretariat by April 15, 2025. Ongoing monthly monitoring meetings will continue to evaluate market conditions, compliance levels, and progress on compensation, highlighting OPEC+’s disciplined approach to supply management. Production penalties, ranging from 200,000 to 500,000 bpd for past overproduction will remain in effect until June 2026.

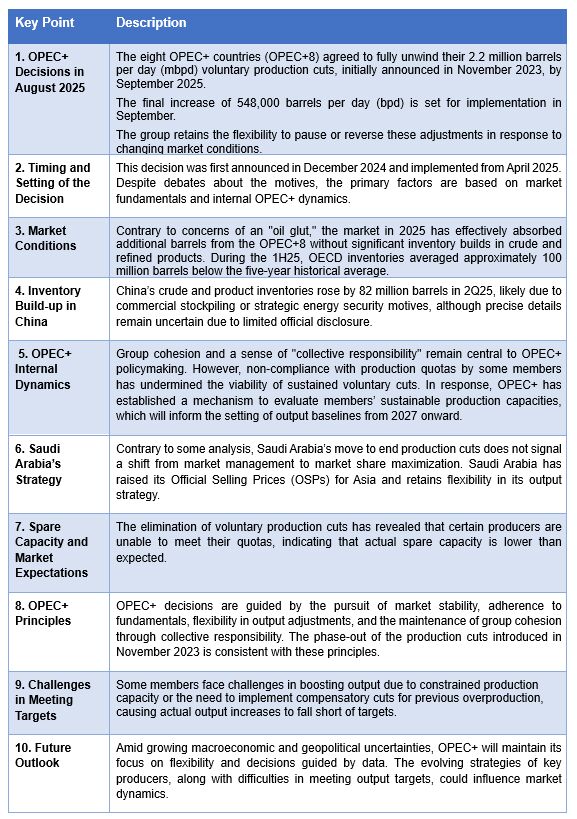

Key Points and Insights

The following table summarizes key points from the analysis, drawing on market dynamics, internal OPEC+ strategies, and future outlook:

Afshin Javan- Senior Energy Economist Analyst

Your Comment